Cipher Pharma Quick Update - $CPH.to

Quick update after Q2 2023 & recent SIB

Last one of my quick updates. Late getting this one out.

CPH released their Q2 2023 numbers and we got a couple of data points. They recently announced an SIB of $6 million between $3.95 - $4.75.

Shares were range bound for about 10 months until it recently broke the $4 mark.

Quarter Notes

Nothing good or bad about the quarter from my standpoint.

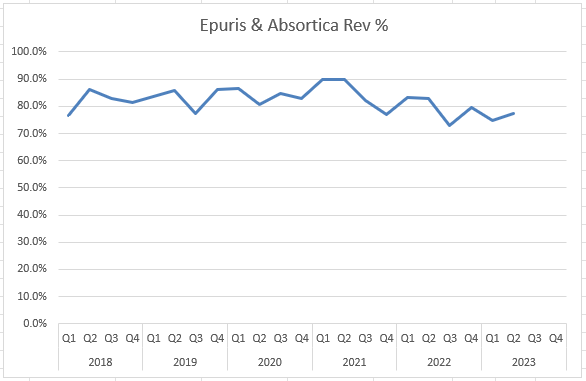

Epuris was down a bit from last year’s very tough comp.

Absortica seen some market share gain this quarter.

I’m hoping this marks the end of the decline for Absortica.

Generated 2.9 mil in cash this quarter.

Cash balance now at 36 mil USD.

Epuris launched in Mexico in May and they are receiving revenues now.

MOB-015 obtained European approved during the quarter.

Derisks this for getting approval in Canada.

Full enrollment in phase 3 trial to be completed by year end.

CF-101 was given a positive view for phase 3 trials.

FDA wants 2 trials.

Once approved Canfite will submit marketing materials.

Call Notes

No update on potential M&A.

Mexico market for Epuris is large, although data is hard to come by.

They have the potential to launch some of the legacy Galephar assets in Mexico as well, though there was nothing to report at this time.

Sun launched Absortica LD which is a slightly lower dose of Epuris.

They weren’t concerned long term about this gaining significant share.

They are in discussion with Health Canada regarding this.

Health Canada approved the launch so I’m not sure they get anywhere.

They noted that this may cause the dermatologists to do some extra calculations and most will just stick to Epuris.

Closing Thoughts

A couple of large catalysts have been slowly marching forward (Epuris launch in Mexico, MOB-015 and CF-101), some things are stuck (M&A) and one new concern for me (Sun launching Absortica LD in Canada). I am not sure if they net each other out in the short term, but I feel the long term thesis is still here.

We have Abosrtica in the US generating minimal revenue and now Epuris will have to compete with some version of Absortica in Canada. Based on the language and tone of the call, I have less confidence in Cipher and Sun able to come to an agreement on Absortica in the US when the current one expires at end of 2024 and 2026.

In March 2022, the Company entered into the Absorica Amended and Restated Agreement. Under the terms of the Absorica Amended and Restated Agreement, Cipher and Sun agreed to extend Sun's exclusive right to market, sell and distribute the isotrentinoin product portfolio, Absorica and Absorica AG in the United States through December 31, 2026 and Absorica LD through December 31, 2024.

Depending how this unfolds, in In the immediate to medium term 70-80% of their current revenue is less certain than it was a year ago. They have now entered Mexico with Epuris so that may be enough to offset some or all of the potential decline from the above. In the long term the commercial value of MOB-015 and CF-101 is quite large relative to the market cap of the business.

This doesn’t take into account the large cash balance that could be utilized productively. As they have with the recent SIB announcement.

In my opinion, I think risk has gone up a little for CPH. CPH is a large position for me and given it’s liquidity I need to be mindful of the risks. I am going to investigate Absortica LD in the US where it apparently didn’t do that well based on the comments on the conference call. If anyone has any information on this and is willing to share, I would appreciate it.

Please share this with anyone who you think would find it interesting.

Thanks for reading.

Dean

*long CPH.to

If their growth assumptions are hit, I think Cipher trades to at least $16 CAD/share at a 8x run rate of FCF. Size puts us into the realm of small cap funds. Add net cash + buybacks, and we could be looking at a $25 stock here in a few years.