Cipher Pharmaceuticals Inc Quick Update - $CPH.to

Update after Q1 2023 results

Cipher reported Q1 2023 last week. Here is my quick recap. They report in USD.

Price: $3.50 CAD

Market Cap: 63.7 mil USD

EV: 30.5mil USD

Business Highlights

Revenue down 10%

Ebitda up 3%

Generated over 3 mil in cash before working capital adjustments

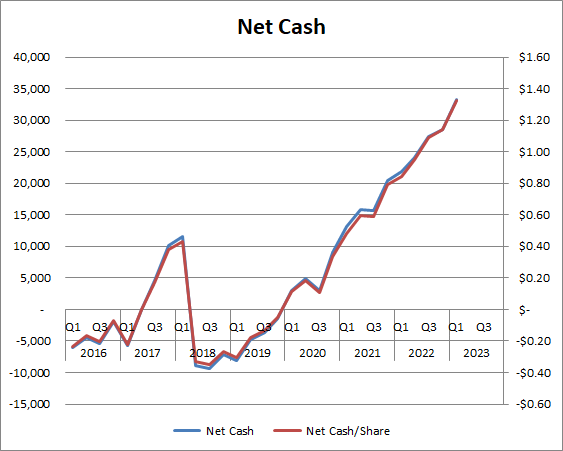

Net cash is now over 30 mil USD

The company continues to run very lean and generate more cash than they can deploy. The downtick in revenue was from lower Absortica licence revenue (0.95 mil vs 1.40 mil) and lower Epuris product sales (2.7 mil vs 3.1 mil). Incrementally, the Absortica revenue is not really material. At his rate they may actually generate more revenue from Lipofen than Absortica this year.

Call Highlights

Still working on their pipeline, namely CF-101 and MOB-015.

With cash and credit facility they have access to nearly 70 mil USD.

May see increase in revenue from Aggrastat and Durela in 2023.

They are looking in both Canada and USA.

Should be generating some royalties from Mexico sales of Absortica.

Anticipate utilizing the NCIB once blackout period has passed.

Cipher switches in and out of my largest position, so I’m definitely following it closely. CPH trades at less than 5x FCF. I’m not sure how much M&A will produce in terms of earnings and cash flow at this point, so I haven’t used it yet in my valuations for CPH. The (excess) cash is worth something, I’m just not sure how much.

I continue to sit on my hands and hold my shares.

Thanks,

Dean

Thanks for the update. The combination of drop in Epuris and increase of cash as a percentage of the market cap make me nervous. This is now almost entirely a story about what management is going to buy with their overcapitalized balance sheet

Almost a year ago I was going back and forth between Cipher and Medexus... I feel in love with treosulfan and went with Medexus. My first “well that was stupid” mistake. Definitely looks good if they can find good places for that cash.