Cipher Pharmaceuticals Inc Update - $CPH.to

Cipher reported Q1 2022 and though it wasn’t anything eventful, I am holding myself to account to discuss my larger holdings publicly. CPH gets essentially zero attention because they don’t produce hydrocarbons and there is nobody comparing their PE to $KO.

License Products

Absortica revenue declined (as expected) to 1.4 mil for the quarter. It has been 1.4, 1.6, and 1.4 mil for the last 3 quarters. Potentially this is the bottom on Absortica revenue. Q2 2022 of 2.4 mil is the last “tough comp” on Absortica revenue.

Lipofen has been showing some recent strength and revenue grew to 0.7 mil from 0.3 the year before. They announced a new agreement with ANI in Sept 2021 for the next 5 years. Lipofen is a cholesterol drug, so I’m assuming it should be fairly agnostic to the overall economy.

Commercial Products

Epuris totaled 3.1 mil vs 2.6 mil last year. Nice to see the continued strength in the product. They have average almost 2.9 mil in revenue per quarter for the last ttm.

Other Commercial products had a negligible impact yoy.

Cost Cutting

Since taking over as interim CEO, Mull has continued to cut expenses as shown below. I’m not sure how much lower they can go from here, although the continued focus on opex has me confident that they will continue to generate cash at this top line level.

It should be noted that even with the lower opex line, they company has been able to negotiate license agreements with their existing products.

NCIB

Unlike most companies that announce an NCIB and barely execute on it, CPH has continued to buy back shares. There are about 5% less outstanding shares this quarter vs last year.

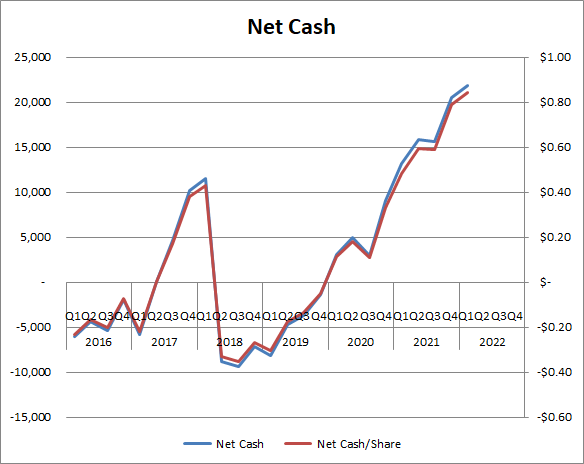

Balance Sheet

Net cash hit another record this quarter and stands at approx $0.84 (USD) per share vs the share price of about $1.77 in USD.

Looking ahead

Given the capital allocation execution from the interim CEO, I am fine parking my capital here. I would like them to acquire a company/product that would diversify their revenue stream as they are heavily reliant on Epuris at the moment. I am expecting them to buy something that isn’t sexy at a reasonable valuation. I would be disappointed if they don’t announce something in the next 2 quarters on this front. A purchase that would diversify their revenue stream should result in a higher multiple.

I would also expect the buybacks to continue. I wouldn’t be surprised by an SIB, but I’m not expecting it at this point.

I am modeling essentially a flat year for the company. Absortica revenue declines likely being made up by Epuris and Lipofen this year and maybe even some small growth in the top line. This of course is assuming that they don’t commit any significant capital to their current pipeline. Of course if they did, it would likely be a good thing.

The company trades around 5x FCF and under 3x EV/FCF. I think there are multiple ways to win here.

Anyone have any thoughts on CPH?

Thanks,

Dean