DIRTT Environmental Solutions Q4 2025 Update – DRT.to

A Different DIRTT Heading Into 2026

Disclosure: I own shares in DRT. I am not a professional. Please do your own due diligence.

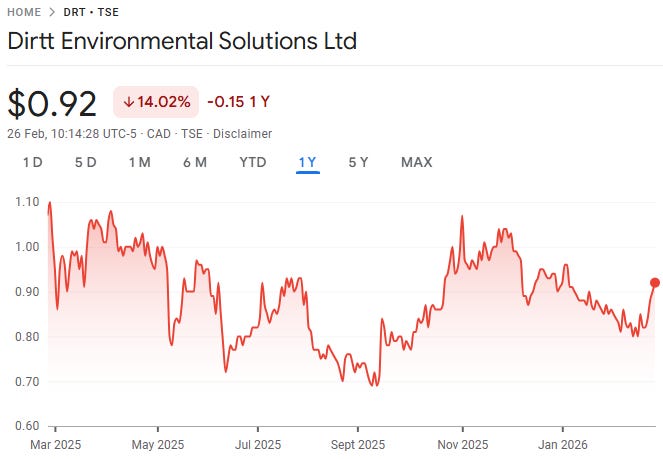

Price: $0.92 CAD / $0.66 USD

MC: 125 million USD

EV: 130 million USD

1 year performance: -14%

DIRTT reported last night and held a call this morning. Results were ahead of estimates on both the top line and EBITDA. The stock is up 2.2% at time of writing.

*all numbers in USD unless stated otherwise

Quarter Recap

Revenue of $50.9M (+4% YoY) vs $48.9M in Q4 2024.

Full-year 2025 revenue was $168.9M (-3% YoY vs $174.3M).

Gross profit of $18.6M with gross margin of 36.6% vs 35.9% last year.

Sequential improvement from 30.4% in Q3 2025.

Adjusted EBITDA of $6.2M (12.1% margin) vs $5.5M (11.2%) last year.

Breakdown of different business segments

Q4 revenue mix:

Product revenue: $49.3M (~97%)

Service revenue: $1.6M (~3%)

Full-year 2025:

Product revenue: $164.1M

Service revenue: $4.8M

Other Relevant Data Points

December 2025 was the highest revenue month in over two years (management commentary).

5% price increase and 3.5% tariff surcharge implemented earlier in 2025 supported Q4 revenue.

Transformation Office established in early 2025 to streamline processes and improve productivity.

Rock Hill facility lease terminated; $2.3M non-cash impairment recorded, partially offset by $0.9M gain on lease derecognition.

Additional $0.7M impairment related to Phoenix facility ROU assets.

Convertible debentures (C$16.6M) repaid January 31, 2026.

Secured C$15M committed BDC facility (C$5.5M received to date).

NCIB renewed allowing repurchase of up to 9,593,878 shares.

2026 guidance: Revenue $194–209M; Adjusted EBITDA $26–31M.

Conference Call Notes

Anything worth calling out in the conference call

Management described Q4 as a “return to normalcy” in sales and earning power.

Sequential gross margin recovery highlighted as tariff mitigation began to take effect.

Transformation Office initiatives expected to continue through 2026.

Litigation with Falkbuilt remains ongoing; trial commenced February 2, 2026. There was no mention of how this is going on the call.

Guidance reflects current tariff assumptions; company will update if impacts become quantifiable.

Valuation

DIRTT is trading at 4.5s EV/EBITDA using the guidance they provided. Mid point of guidance indicates about a 20% top line growth from 2025.

Closing Thoughts

This was a noisy GAAP quarter with quite a few moving pieces. Q1 2026 had some pretty big changes.

Rock Hill facility lease terminated (effective Dec 30, 2025)

$2.3M non-cash impairment recorded.

Manufacturing footprint fully consolidated.

Removes legacy cost drag going into 2026.

Executive Leadership Reset

COO (Rich Hunter) departed.

He led manufacturing turnaround and defect reduction phase.

New CTO (Aaron Merkin) appointed.

Former Fortive CTO; background in tech-enabled industrial transformation.

Signals shift toward technology optimization and ICE software leverage.

Capital Structure Cleanup

C$16.6M convertible debentures repaid (Jan 31, 2026).

BDC financing secured (C$15M committed; C$5.5M drawn so far).

Falkbuilt Litigation Began

8-week trial commenced Feb 2, 2026.

Governance Stabilization

Support & Standstill Agreement signed (Feb 13, 2026).

22NW (largest shareholder) and 726 Entities (Briger family vehicles) aligned with management.

Jeremy Gold (Briger Family Office) appointed to board.

Voting commitments and standstill provisions in place.

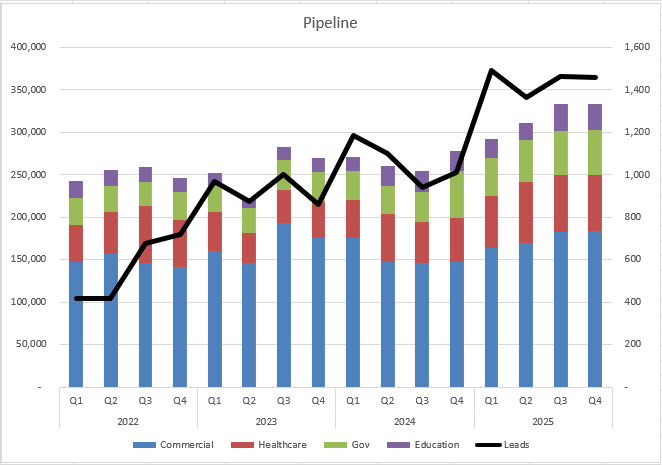

The leading indicators both inside the organization and outside are strong. Below is the pipeline.

Given how they had to remove guidance last year after due to the tariff impacts, I don’t think they consider issuing guidance if they had any uncertainty about hitting it. 2026 should be a good year for DRT.

Thanks for reading my work.

Dean

long DRT.to