Ensign Energy Services Q1 2025 Update - $ESI.to

Not bad. Focusing on paying down debt.

*Disclosure: I own shares in ESI. I am not a professional. Please do your own due diligence.

Price: $2.11 CAD

MC: 390 million CAD

EV: 1.4 billion CAD

1 year performance: -8%

ESI reported this morning and held a call. Results were roughly in line with of my expectations and the stock was up 11% today.

*all numbers in CAD unless stated otherwise

Quarter Recap

436.5 million revenue vs 431.3 million last year

Up 1%

102.4 million adjusted EBITDA vs 117.5 million last year

Down 13%

Geographical Mix

Canada - $152.0 million, 35% of total

United States - $205.8 million, 47% of total

International - $78.7 million, 18% of total

Capex at 37 million

down 30% yoy

down 49% if you include asset sales

about 3 million in growth and 35.7 million in maintenance capex

2025 capex budget at 164 million

Call Notes

Had some frictional costs in the US for deactivation and reactivation of rigs

Despite the headlines, they didn’t seem overly concerned about the business

More rigs needed to hold production in US here

Started beta testing of AutoDrillingMax

100-110 drilling rigs and 50-60 well servicing rigs operating daily both sides of the border

US near term headwinds, expect to get better in 2026

Expecting a couple of rigs to come off in Q3

I got the impression that International will net out to being about flat this year

750 million in booked revenue

1/3 of rigs under contract

25% of contracts on a performance basis

Expect real estate disposal in 2025

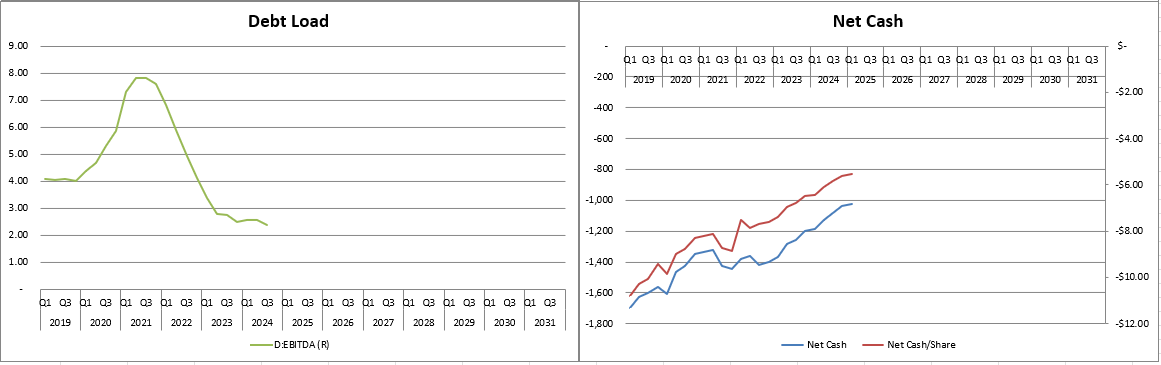

Still expect around 200 million in total debt repayment in 2025 and 600 million from 2023-2025

Given where they are at after Q1, I have them attempting to pay another 140 million (minimum) for the remaining 3 quarters this year

Valuation

I have them at 3.3x EV/ttm EBITDA. Not sure what the rest of 2025 holds for OFS cos, so I’m hesitant to make too many estimates.

Closing Thoughts

I thought the quarter was as good as can be expected. As we get used to whatever activity levels look like, I think capital slowly returns to the industry and the valuations creep higher.

ESI has a large debt repayment story. They have been making strong progress at deleveraging the balance sheet and I expect this to continue.

ESI has more of a direct exposure to activity levels than some of my other OFS cos. I think this point in the cycle is not a bad place to build a position. I own ESI in a basket of OFS cos. I added a bit to the name under $2.

Thanks for reading my work.

Dean

* long ESI.to