FAX Capital - $FXC.to

Very simple idea here.

Background

From their site:

FAX Capital (TSX:FXC) is an investment holding company. We are a permanent capital vehicle, allowing us to take a true long-term approach to investing, providing the foundation to maximize compounding and to hold quality investments indefinitely. We have full flexibility in our investment mandate, allowing us to invest in public and private companies, across the capital structure, and in a wide variety of industries. We are active owners, working collaboratively to augment already strong management teams, leveraging our experience in business building and capital markets expertise. We have a deep and demonstrable track record of value creation, both as operators and as investors.

The company was an old gold mining shell that raised the majority of the capital in late 2019 at $4.50. Fax Investments supplied 120mil and a further 70mil was provided by outside capital. The subordinate voting shares issued where also given a 2 year founder warrant which Fax Investments didn't get. Directors and senior officers participated in 553,667 or 3.56% of the issued shares.

Voting control for this company is controlled by Fax Investments which is controlled by the Driscoll family. Fax Investments owns 63% of the outstanding shares (which includes all the multiple voting shares). The Driscoll family is most known for Sentry Investments which was sold to CI for 780mil. They managed to build up to 19bil in assets before the sale (1997-2017).

The goal was to be fully invested in 12-18 months from when they raised capital in late 2019.

The ideal portfolio allocation is 60-80% in 10-15 public companies, and 20-40% in private companies. At Sept 30, 2020 about 50% of assets where in cash.

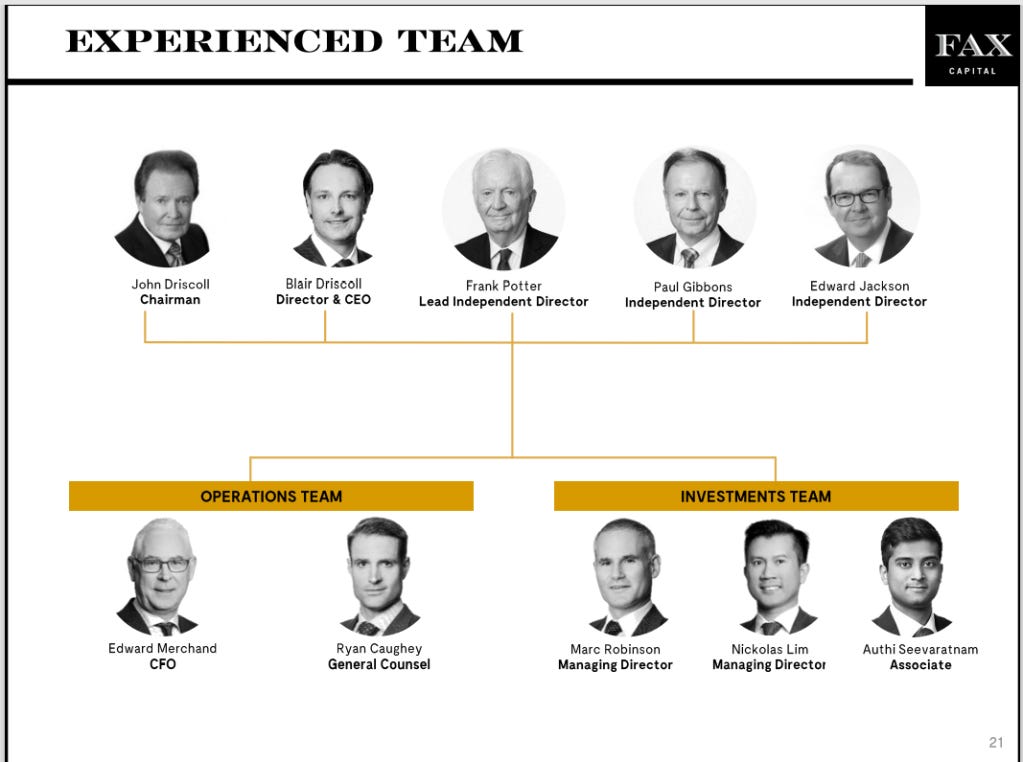

Management

The Executive team

CEO is Blair Driscoll (son to John Driscoll)

takes no salary

he is also the President and CEO of Fax Investments

CFO Edward Merchand

General Counsel Ryan Caughey

Board

The Board is chaired by John Driscoll (78)

He is on the board of some other public companies and seems well connected

Lead Independent Director is Frank Potter (83)

Blair Driscoll (38 - same age I'll be this year in case you are wondering)

Edward Jackson (63) - independent

Paul Gibbons (62) - independent

Independent board members combines own 105,000 shares (0.2.%) and about 95,000 founder warrants

Investment Team

Marc Robinson - Managing Director

most recently was he was the sole portfolio manager of LDIC North American Small Business Fund which returned 17% annually from mid 2016 to April 2019

Nickolas Lim - Managing Director

most recently from Hamblin Watsa Investment Counsel, a subsidiary of Fairfax and Brookfield Asset Management

Authi Seevaratham - Associate

was an analyst Cambridge Global Asset Management

They committed a minimum of 2% of the offering

LTIP based on 6% annual CAGR

There is no management fee

The investment team owns 179,000 shares subordinate shares, 186,000 founder warrants and has further exposure via restricted and performance shares

Investment Principles (from their website)

Will invest with a long-term view;

May invest in both public and private companies;

Will take a concentrated approach to portfolio construction (which is initially expected to include 10-15 target companies);

May invest across the capital structure, tailoring its investments, where appropriate, to the needs of portfolio companies including through equity, debt and/or hybrid securities;

Will invest in high-quality businesses or those that have the potential to be high-quality businesses;

Will work for continuous improvement in the performance of portfolio companies through active ownership and the leveraging of its industry experience, business contact network and financial strength; and

Will seek to promote and encourage best-in-class governance practices in the portfolio companies.

Their currently disclosed investments

Here is slide from their most recent presentation showing the thesis behind their public company investments. They have also purchased a controlling interest in Carson, Dunlop & Associates, their first private purchase. The purchase of Carson, Dunlop & Associates is expected to close in Q1 2021.

ISC is a familiar name that was discussed here.

I have also followed Hamilton Thorne for about 5 years and really respect the management team and business.

Points hasn't performed great since their initial purchase given the pandemic, but subsequent adds have done well relative to the index.

People Corporation is being bought by Goldman Sachs.

Their book value growth has grown over the last year. It has outpaced the TSX Composite while having lots of cash dragging down performance. I have tried to track their purchases (and addition purchases) of their disclosed investments. They are on average beating the TSX by a fairly wide margin.

Peers

Closed end funds typically trade at a discount. How much of a discount depends on many things (share structure, ownership, liquidity, the market's perception of the operators, etc). There are a couple of peers that I think are relevant for Fax. I will let the reader decide if these peers are relevant.

Here is a graph of Price to NAV

Onex is huge and may not be a great comparable

Pender growth has done well and should be recognized for their performance on book value growth

They currently have about 4% in cash

URB.A has the largest discount and has for a long time

PNP was hard to find information on so take the valuation with a grain of salt

CYB has 20% of NAV in Edgepoint

Edgepoint funds manage to beat their benchmark fairly consistently

Structural costs that I don't have

It's tough for anyone to outperform the market over a long period of time. There is no doubt that the investment team that is allocating capital is more connected, intelligent and resourced than I am. However, there are some additional costs that FXC has that I don't. Some additional frictional costs to the structure are:

fees paid to directors - this was 300k in 2019

salaries paid to execs and investment team

they have to disclose purchases

termination agreements with CEO and CFO

some positions are not overly liquid

Other Relevant Links

YT vid they did with Dhalla Wealth Management

fax_investor_presentation_-_q320_finalDownload

Investment Thesis/How to make money

In my opinion, there are a few ways to look at investing in a closed end fund or something similar to FXC.

You are looking to allocate capital to strong allocators for a long period of time based on NAV growth. It can reduce risk in a portfolio if (despite the hurdles) the NAV grows quicker than if you put the money to work by yourself.

It diversifies (and potentially lowers volatility) into other businesses or sectors that you can't analyze or don't have access to (private businesses). This can have merit as well if you are looking to diversify "style" or "investment strategy". I am guilty of struggling to pay up for high quality businesses with strong management and it has cost me dearly.

You are comfortable with the structure, team, investments, etc. but you feel the discount to NAV is too large. FXC (and others) will buy back shares if they feel the discount is too large. There are of course restrictions and can also be self-defeating as it reduces liquidity in what is already an illiquid company. FXC has bought back some shares at a discount.

At this point, I'm not sure which one this is for me at this point. I like the companies they own and that they are able to partner with the businesses. With my cash position climbing, I was fine taking a small position. Hat tip to Graham for the idea and the help.

Risks/Things to get comfortable with

NAV could drop

NAV may not climb as quick as the market does

Price to NAV could widen

There could be some friction between the investment team and management

FAX Investments controls the voting decisions

I think incentives are aligned enough for me to be comfortable. No one wins if NAV declines. I'm operating under the assumption that deploying the cash could be a decent catalyst to close the discount to NAV.

Anyone have any opinions on FXC or the other companies mentioned?

Thanks,

Dean

*the author has a (small) position in $FXC.to at time of writing.