Firan Technology Group Quick Update - $FTG.to

Happy Valentine's Day from your favorite Canadian powerlifter.

It's been awhile since I spent some dedicated time on Firan, so I thought I would provide a quick update. You can see my last post way back here and the original post from 18 months/3 covid lifetimes ago.

Since the original post shares are up 30% vs TSX being up 40%. You can see FTG outperformed better for a brief period and has since slid below the TSX.

Since the last update shares are down 22% vs TSX up 10%.

Firan has been more than mildly affected by the pandemic. Demand for commercial aerospace plummeted fast as the world came to the conclusion that the travel restrictions would be around longer than a few months. Their operations have been affected by staffing issues due to covid and related isolation and testing guidelines. As well, they are impacted by various global supply chain issues. Their last quarter was a good example of how vulnerable they are. Despite all these challenges the company has persevered and generated cash.

Shared have actually been stronger than I would have expected after the soft quarter. Could have something to do with reopen expectations or worry about war between Russia and Ukraine.

Looking ahead

FTG doesn't seem cheap based on trailing earnings which are depressed due to the reasons listed above. When I look at this business, I want to try and get an idea of what "normal" looks like after we all turn in our epidemiologist badges and focus on whatever else comes next. We can use the past as a guide to see what the future could look like. When I say "normal" I don't mean in a few quarters, I mean in a few years.

Fiscal Q3 2018 to Fiscal Q1 2020 an average of 105 mil in revenue, 10.5 mil EBITDA and 6 mil in EBIT. If we return to those numbers than FTG is trading at 4.3x EV/EBITDA and 7.3x EV/EBIT. They purchased Colonial Circuits in July 2019 which added 7-9 mil in revenue to the business that isn't fully included in these numbers.

In the quarter immediately preceding the pandemic they did 112 mil in revenue, 15 mil EBITDA, and 10 mil in EBIT. If those numbers are in the cards then FTG is trading at 3x EV/EBITA and 4.5x EV/EBIT.

My estimate is that full cycle EBITDA is around 12 mil. Taking some estimates on cash flow conversion and maintenance expenditures, I get 6-7 mil in steady state earnings. This gives us 10x such earnings and 7x EV/estimated earnings. Of course, there are a bunch of underlying expectations here.

Of course this assumes that not only will revenue return, margins will be comparable. There's quite a few assumptions baked into those numbers. How likely is FTG to return to the good old pre-pandemic days? I'm not sure. I do know that we are likely to see stable defense budgets from major governments over the next couple of years. Commercial aerospace should make a comeback this year and next as there is a bunch of pent up demand for travel. Although business travel may be impacted due to all us getting used to virtual meetings. Boeing and Airbus have slowly been increasing deliveries from the trough in business activity.

Looking to the asset base to provide some downside scenarios we can see that FTG has traded cheaper than it is now relative to the tangible assets in the business. Although FTG was not generating as much cash in those days as it did before the pandemic. Having said that, the backlog has not returned to pre-pandemic levels, at least not yet.

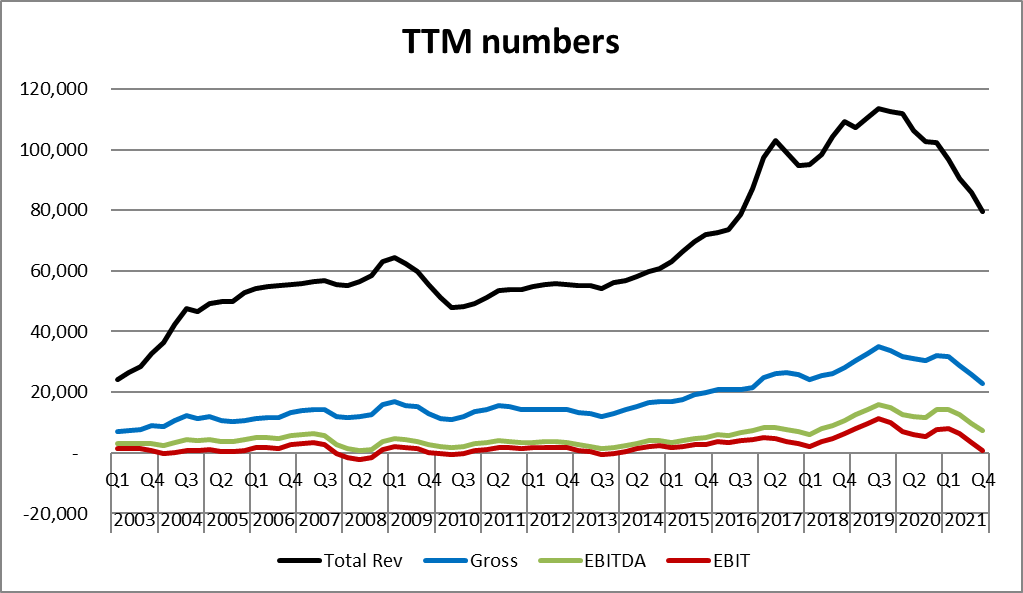

You can see how the P/TB ebbs and flows with the performance of the business. This is looking backwards and the business is quite different from a decade ago. Looking at the income statement may be helpful.

Several years of sideways performance is not uncommon. The profitability of the business has followed revenue. It's nice to see gross margins relatively stable and generally in an uptrend.

Risks

Some risks that I think are worth noting are:

The economy may not reopen if we have another variant.

Supply chain issues could drag on longer than anticipated.

Labour disruptions due rising inflation.

Input costs increasing faster than they can raise prices.

They could let the cash sit on the balance sheet too long and the use of EV may not be appropriate.

We may never get back to prior activity levels even if covid slowly fades in the background.

Given how well the company has done, there is some key person risk with the CEO.

Summary

FTG is a company that earns a reasonable return on the capital throughout a full cycle. They have grown per share numbers at a reasonable rate as well.

FTG seems like a decent bet here. The CEO owns 10% of the company, is reasonable compensated and seems like a strong operator. The company has been through a few cycles and knows how to make tough decisions without a ton of consulting from a major accounting firm. I see the recent headwinds turning into tailwinds as the economy reopens. They also have almost 18 mil in net cash or $0.73 per share. This added cushion can be deployed in a productive manner rather than sit on the balance sheet. I don't own shares but I am digging in further on the business.

Anyone else have some FTG or an opinion on the business.

Thanks,

Dean

*no position at time of writing, but that may change.