Foraco Q2 2024 Update - $FAR.to

Quick update after Q2 2024

*Disclosure: I own shares in FAR.to. I am not a professional. Please do your own due diligence.

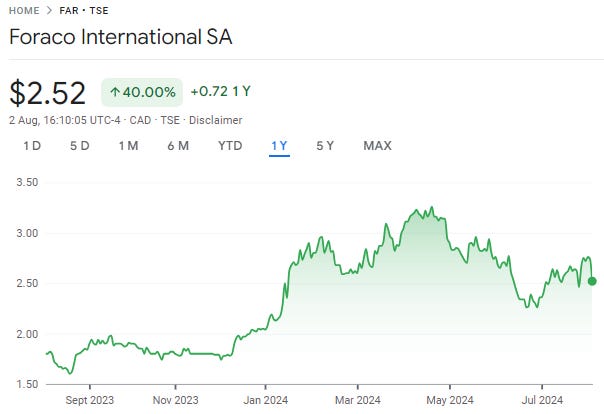

Price: $2.52 CAD/$1.99 USD

MC: 200 million USD

EV: 276 million USD

Yield: 2.3%

1 year performance: +40%

FAR reported yesterday morning and held a call early in the day. Results were well behind my expectations and the stock was down 8%.

*All amounts in USD except per share numbers.

Quarter Recap

Revenue was 77.9 million vs 100.1 million.

Down 22%.

EBITDA was 16.4 million vs 23.8 million.

Margin of 21% vs 23.8%.

Rig utilization was down to 40%.

Some reasons for the weakness were:

Early winter (at least compared to last year) South America.

Juniors not getting financing in South America.

Exiting some countries in West Africa as EMEA revenue was down 60%.

Call Notes

They are pivoting to more stable jurisdictions and (hence) to seniors and Tier 1 customers.

They are mobilizing the rigs that are idle in West Africa and South America.

The market in Latin America is stable overall, the winter impact makes for a tough comp from last year.

The juniors were also an impact.

There are some newer rigs headed for Australia that will help the top line.

There was no explicit guidance given on timing when revenue will grow again. The remobilization will not happen overnight, so it sounded like we should expect a weak Q3.

Valuation

I have lowered my expectations for the remainder of 2024. I have FAR at 3.4x EV/2024 EBITDA and closer to 3.2x EV/2025 EBITDA. This would equate to 7-8x EV/”normalized” FCF.

Closing Thoughts

I am still a little fuzzy on the mix of the impact of the timing of winter, junior financing and West Africa. I was under the impression that EMEA revenue had bottomed after they exited Russia. I was wrong. EMEA revenue was already the lowest geography going into the quarter.

There was some strength in North America and Asia-Pacific that offset the weakness. The new CEO had mentioned that he had a focus on North America, so it was nice to see the execution.

Such is the risk with such businesses that rely indirectly on the capital markets. I was caught flat footed. GEO.to has done something similar, but I was assuming that FAR customers were less affected by the capital markets.

I will hold my shares here and digest the quarter. My poor understanding of the business has been bailed out by a dirt cheap valuation and buoyant gold market. I still think the business is decent quality and that they have room for multiple expansion if we continue to see rotation into smallcaps.

Thanks for reading.

Dean

* long FAR.to