High Arctic Special Situation - $HWO.to

Cuz I'm ready to get hurt again

Every few years I try a special situation and more often than not, I end up losing money. Thank fully the pain only lasts a few years and I manage to get through all the stages of grief just in time to try again.

Enter High Arctic. I’ll go over my best guess at valuation and then the associated risks. Please feel free to comment if you feel I have missed something as I would really appreciate the feedback.

I owned HWO going into the news and added as shares have not really responded to the news.

Ticker: HWO.to

Price: $1.19

Shares Out: 48.7 mil

Market Cap: 58 mil CAD

EV: 13.2 mil CAD

The Set-up

HWO is an OFS company that has a mix of assets in Papa New Guinea and North America. They were once an income trust that distributed their earnings (mainly from PNG) to shareholders on a monthly basis. During the slowdown in 2015/16 in O&G they purchased assets from Tervita for 42.8mil. They have since sold the Well Servicing assets and have a large amount of excess cash on the balance sheet.

HWO announced on it’s Q1 2023 first quarter results that they intend to return capital to shareholders, spin off the International (PNG) business and leave the remaining company listed in Canada with the associated NOLs. There essentially 3 different pieces here that you are getting in today’s price. I have not counted any monthly dividends as it is essentially returning the stated cash. I also have not counted any cash generated by the business. They are expecting the special meeting to be held before the end of September 2023.

I have taken a stab at a low/high or pessimist/optimist range.

Low End

Return of capital to shareholders

PNG portion of the business based on assets

Canadian shell remainco with low value for NOLs

High End

Return of capital to shareholders (same as low end)

PNG portion of the business based on potential earnings

Canadian shell remainco with higher value for NOLs

1) Returning Well Servicing Proceeds to Shareholders

This is the easy part. Return of capital to shareholders from the recent sale of Canadian Well Servicing Division. This is a tax efficient way to distribute the excess cash to shareholders. This is valued at 38.2 mil or about $0.78/share.

2) PNG/International spin off into private co

The board feels that a spin off of the PNG business into a private company would allow senior management to focus on the PNG business alone. I can see the point as the market does not give much value to the PNG business at the moment. It looks like PNG is setting up for a multi year increase in business activity. On the Q1 call, they had mentioned that they don’t expect to list this on any major exchange and didn’t commit to providing a liquidity option to current shareholders. This is the largest concern for current shareholders. I’m looking at this two ways - asset based and earnings based. They did say that they don’t anticipate any major capital being needed to get all the rigs operational.

Low End - PNG Asset Based

On Q1 2023 the PNG business had assets of 68.4 mil that is split between current and long term assets. There isn’t a specific breakout of the liabilities for PNG vs Canada so I have to make some assumptions. I am going to assume that 50% of the liabilities listed in Q1 2023 are for PNG. This equates to 9 mil. This leaves an equity value of about 59.4 mil. I’m going to use a multiple of 33% of equity value here. I get a value of 19.6 mil or $0.40 per share.

High End - PNG Earning Based

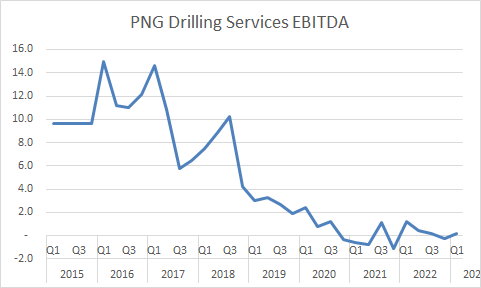

There will need to be some assumptions to estimate the potential earnings from PNG. They rig structure has changed over time and the services provided in PNG is not the same as the past. In Q1 only 1 rig was operating for part of the quarter (rig 103) and will remain under operation until the end of the contract in July 2025. Revenue from PNG over 8 mil with over 6 mil from rig 103 operating only part of the quarter.

HWO has disclosed segmented results geographically all the way back to 2007. They have split out the various divisions from 2015 onward. Taking the average quarterly revenue of almost 25 mil for PNG and a 20% EBITDA margin gets us 5 mil in EBITDA per quarter. There have been many years with EBITDA from PNG Drilling Services was above this by a wide margin and that doesn’t include additional EBITDA from Ancillary services in PNG which is made up of some rental equipment.

Taking the 5 mil and annualizing it we get 20 mil. I slapped a 3x EBITDA multiple on it and get a value of 60 mil or $1.23 per share (pretty much the share price today).

3) Remaining Canadian Assets

The remaining assets will continue to be listed. These consist of 126.7 mil in non-capital unrecognized losses, 39.6 mil in capital losses, Team Snubbing convertible note, HWO’s share of the Team Snubbing equity and some cash that I have assigned after the distribution. The non-capital losses expire from 2027-2042 and the capital losses carry forward indefinitely. Team Snubbing in Canada’s largest Snubbing provider.

I tried to come up with a range of outcomes here for the this piece. I feel both are conservative, but realistically I don’t have a ton of insight into how much the NOLs would be worth. I played around with some DCF assumptions for the NOLs and all of the assumptions came in higher than the value I have assigned here, so I will use the more conservative numbers.

Low End

I really just took the NOLs down to 5% of their value, kept the assigned cash of 5 mil and convertible note at stated value and brought down the Team Snubbing Equity value to 33%. I also took the total value of 24.27 mil and gave it a 66% multiple. I get about 16 mil or $0.33 per share.

High End

It’s the same as the Low End except, I took the NOLs up to 15% of stated value and the Team Snubbing equity to 75%. All the DCF assumptions I used gave the NOLs worth north of 40mil, but I have elected to use the more conservative numbers here. I gave the total value a 75% multiple as well as I assume it would trade at a discount to the NAV. I get 38.9 mil or $0.80 per share.

Summing Them Up

I get a range of $1.52 to $2.82. I feel these are quite conservative estimates particularly for the PNG side of the business which could surprise to the upside by a substantial margin.

Risks

Other than the stated risk of the deal not going through, the largest risk is the potential for no liquidity being provided for the PNG business. Current shareholders could be stuck with a minority stake in a private company without any say in operations or capital allocation. As a microcap investor, I’m accustomed to low/virtually no liquidity but this is even worse.

Currently Cyrus owns 21.9 mil shares or 45% of the common. They have been a shareholder for over a decade and have participated in financings in the past. They have also had board representation in the past as well. They did not indicate how Cyrus intends on voting.

The chair and former interim CEO from July to November 2017 (Michael Binnion) owns 3.9% of the common. He has been on the board since 2005.

My understanding is that they need 2/3 of the votes cast at the special meeting. The last three AGMs there have been around 30 mil votes cast. I’m assuming there will be a few more who wake up for the upcoming meeting, but I honestly don’t know how many. So with Cyrus showing up and voting really puts the ball in their court. I’m assuming in order to get the remaining shareholders to approve they need to provide some sort of liquidity event.

If the deal falls through, we should still see quite a run in PNG revenue by that time and get a better picture of what PNG profitability would be with one rig utilized for several quarters. I think the downside is back the $0.90-$1.00 mark. Keep in mind they intend to distribute $0.78.

Closing Thoughts

I’m not sure how much accuracy is needed with the valuation estimates other than the value is likely quite a bit higher than the current share price. I think the board is looking to monetize the PNG assets before we see a large run in activity levels associated with the PNG business. Total Energy has already committed to spending a large amount to develop LNG assets in PNG. The government seem supportive to developing this as it will be beneficial to PNG.

I am banking on there being at least the option for a liquidity event for public shareholders for the PNG side of the business. It may be way under pricing the potential, but at the share price today (net of the distribution) you aren’t paying much for it. I think even without a decent liquidity even for the PNG biz you are not losing much even if the your capital is permanently illiquid. If I end up holding some random rig assets in PNG after this deal I will be fine with it. We put some dudes on the moon over 50 years ago, I think I can figure a way to get my capital back.

FWIW the current CEO recently purchased $6,500 in common recently. The CFO has resigned. A director that represents Cyrus did not stand for re-election at the most recent AGM. As well, one of the current directors sold $10K worth of stock after the announcement. Mixed signals for sure.

Anyone going to join me on this one? Maybe we can get hurt together and at least I won’t go through the stages of grief alone.

Thanks,

Dean

* long HWO.to

Thanks for the write up. HWO is a top position for me and I will add more if price drops a lot post return of capital. It looks to me like a low risk high uncertainty situation. I assign 0 value to the cdn biz (harsh I know) and the PNG stub post return of capital is trading at what, 0.5-1 x earning? My speculation is they will make the private co structure very unappetizing for retail shareholders and insiders will scoop up cheap shares at the sell off. Let’s see