Mattr Infrastructure Technologies Profile - $MATR.to

My latest position.

*Disclosure: I own shares in MATR. I am not a professional. Please do your own due diligence.

Price: $12.06 CAD

Shares: 66.2 million

Market Cap: 798 million (my pro forma estimate)

Enterprise Value: 1.1-1.2 billion (my estimate post AmerCable acquisition)

1 year performance: -26%

I heard about this one a couple years ago when it was still called Shawcor. I never took a deep dive until it was mentioned more recently on X.

Brian Lancaster and Jason Stankowski on Yet Another Value Podcast

Here is where you can find the company’s investor presentations.

TLDR

MATR (formerly Shawcor) is already well covered so you probably don’t even need to read the rest of the post. I think it’s reasonably priced and has a long runway for per share growth. Management has divested underperforming and non-core assets and the true earnings power of the business will be on full display in the coming quarters. It has a similar profile to Terravest (TVK.to) which has been declared a “compounder” but those with larger brains than my own.

Background

From their MD&A:

Mattr provides a broad range of products, which include flexible composite pipe, fiberglass reinforced plastic (“FRP”) underground storage tanks, stormwater management solutions, heat-shrinkable polymer tubing products and low-voltage control and instrumentation wire, cable and harness solutions.

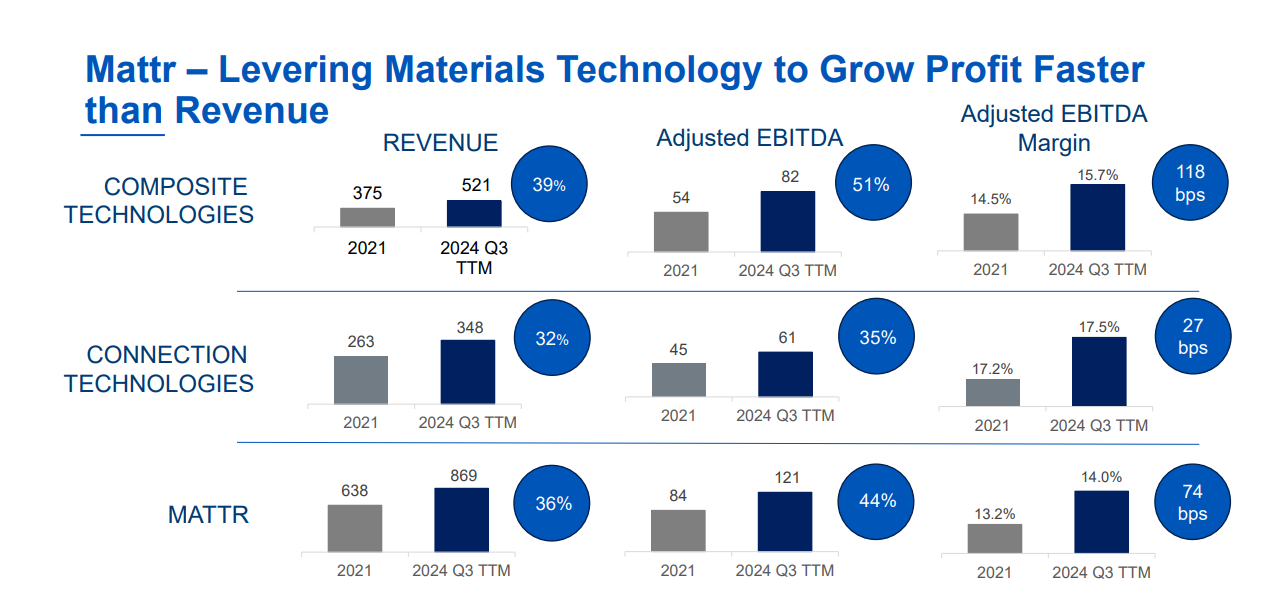

The business is broken down into two segments, Composite Technologies and Connection Technologies. I will not include discontinued operations in the analysis. The following slides are from the January 2025 investor presentation and include the recent AmerCable acquisition.

From the AIF with regards to the divestments:

With the sale of its PPG business completed in 2023, the Company has substantially completed its strategic review process and portfolio transformation. Collectively, the divestitures, cost reduction measures and acquisitions completed by the Company during the three-year period serve to narrow its focus to those businesses that are best positioned to benefit from favourable long-term macro trends while maintaining an efficient operating cost base.

In 2023, as part of its MEO initiatives, the Company began its planned capital investments in the construction of new composite pipe, FRP tanks, and heat shrink tubing production facilities in the US, as well as a new wire and cable facility in Canada, the latter two facilities replacing and expanding the Company’s existing North American footprint for the Connection Technologies segment. In aggregate, once completed, these planned growth capital investments are expected to result in the Company creating at least $150 million per year of incremental revenue generating capacity with comparable margins to those realized in its Composite Technologies and Connection Technologies segments. These levels of outputs are expected to be realized over the 3–5-year period following completion, as the facilities reach efficient utilization levels in accordance with their currently expected timelines.

Business Segments

Before I get into each of the specific segments, I wanted to say a few things about the products here from a high level. When I first looked at MATR I had a hard time understanding how they could earn much above 8-10% ROIC on the businesses on a consolidated basis long term. They felt like a business that in the long run would earn at best a little above their cost of capital. I no longer believe that is the case. As I researched the business, I came to appreciate how much technology is in the various products.

Giving pro forma effect to the AmerCable transaction, the Connection Technologies segment will represent 54% of consolidated revenue on a TTM basis as of June 30, 2024 (an increase from 37% of consolidated revenue previously reported by Mattr for the same time period).

Composite Businesses

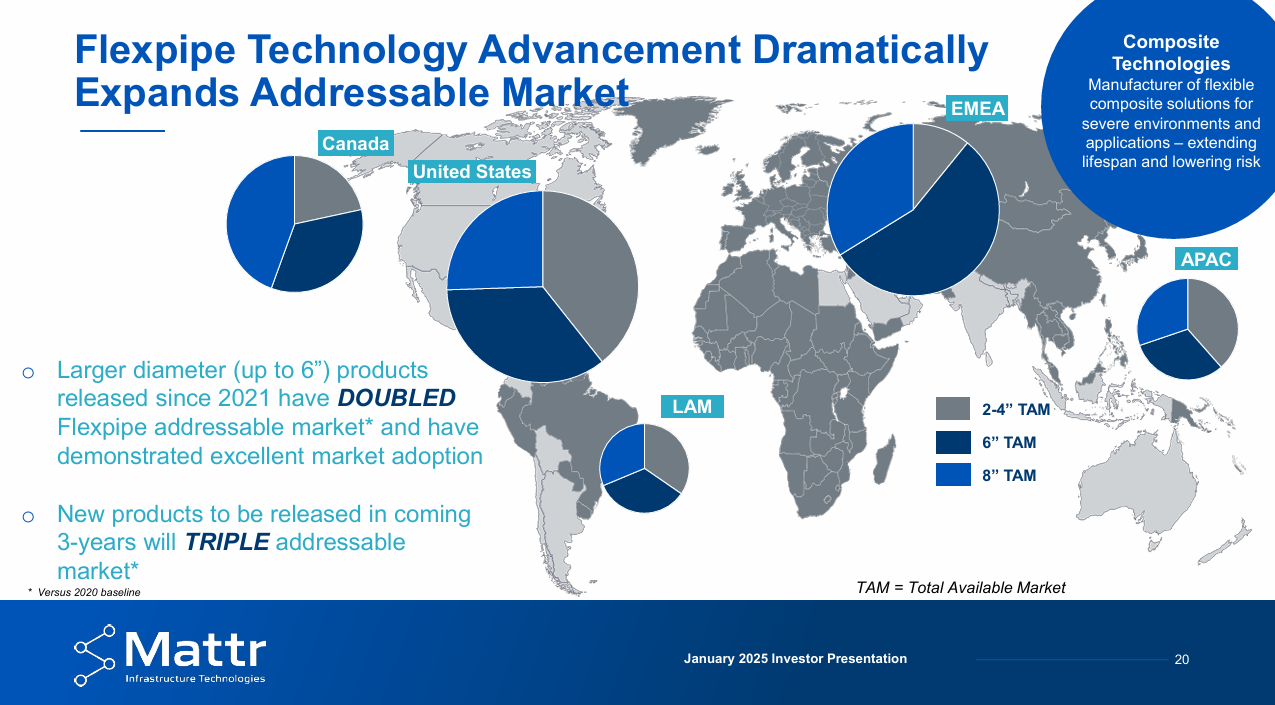

In the composite segment they have the Flexpipe and Xerses brands.

Flexpipe

From the 2024 AIF:

Flexpipe® manufactures proprietary, flexible, corrosion resistant pipeline products which are marketed primarily to oil and natural gas producers in Canada, the United States, Latin America, the Asia Pacific Region, the Middle East, India and North Africa. The division serves its customers through its manufacturing and distribution centre in Calgary, Alberta, and its sales offices and service depots in Alberta, Saskatchewan, Texas, Colorado, Utah, California and North Dakota. In April 2023, the Company announced a commitment for an additional manufacturing and distribution facility, located in Texas, for its Flexpipe® business. These products are marketed and sold internationally through direct sales and a global network of agents and distributors.

The pipe is built to withstand very tough environmental conditions. Composite pipe has taken marketshare from steel pipe consistently over the last decade. I don’t think this will change moving forward.

They sell the pipe globally. The North American revenue has increased for the 9 months ending Q3 2024 even though industry activity was down. The oil and gas side is driven by well completions, so you need to get comfortable with that.

They state that new product introduction should triple the TAM vs 2020.

Xerxes

From the 2024 AIF:

Xerxes® manufactures corrosion free, FRP fuel, water and oil and gas storage tanks, Hydrochain stormwater management systems and 3D glass fabrics. The division serves its customers through proprietary manufacturing and distribution centres located across North America (Quebec, Alberta, Iowa, Maryland, Texas and California), toll manufacturing facilities in Minnesota and Malaysia, and through its sales offices in Minnesota. In April 2023, the Company announced a commitment for an additional tank manufacturing facility, located in South Carolina, for its Xerxes® business and in January 2024, the Company shuttered its tank manufacturing facility in Anaheim, California. The division’s 3D glass fabric weaving manufacturing location in the Netherlands serves the global composite tank market. The FRP tanks are marketed and sold primarily to retail fuel outlets and infrastructure customers across North America. The Hydrochain stormwater management systems are marketed and sold to infrastructure customers across North America, in Europe, Australia and New Zealand.

Their largest customers are fuel station storage tanks. As the existing fuel stations continue to age the tanks are replaced and upgraded. There is of course the reliance on internal combustion engines. The mechanic (and pragmatic thinker) in me feels that we will be using ICE engines longer than most anticipate. The last call had them seem quite confident in demand for Xerxes tanks in 2025.

The latest acquisition related to this part of the business was in 2023, when the Company acquired the assets of Triton, a privately owned provider of storage tanks mainly focused on stormwater management solutions. The Triton product lines are now integrated into the Company’s Hydrochain Stormwater Management business under the Xerxes brand. Triton was acquired for 14.1 million, including a 6.0 million contingent consideration. In 2022 Triton did about 8 million USD in revenue. Call it 1.2x revenue.

The business has successfully expanded into water management as well. The water management revenue continues to grow as they make inroads.

Connections

In connection they have Shawflex and DSG-CanUsa. The recently acquired AmerCable will fall into this segment.

DSG-Canusa & Shawflex

Yes I’m lumping these two together. They are different businesses that have some overlap. It’s a free substack for a reason.

From the 2024 AIF for DSG-Canusa:

DSG-Canusa is a global manufacturer of heat shrinkable and cold shrinkable products for mechanical and electrical insulation solutions. The division also manufactures application equipment and provides integrated systems of equipment and heat shrink products for DSGCanusa manufacturing. Each product meets or exceeds relevant automotive, defense, telecommunications, electrical utility, industrial or original equipment manufacturers’ specifications for performance and safety. These products are sold direct to end users or through distributors and agents throughout North America, Europe and Asia. The division supports its customers for these products through four manufacturing and distribution facilities located in Canada, the United States, Germany and China. In June 2023, the Company announced a commitment for a new manufacturing facility, located in Ohio, for its DSG-Canusa business.

From the 2024 AIF for Shawflex:

Shawflex is a manufacturer of control, instrumentation and low voltage power cables for use primarily in industrial applications and its manufacturing facility is located in Toronto, Ontario. The division is a market leader in Canada with custom engineered and specialty products sold direct to end-users or through distributors and agents throughout North America. Its electrical products meet or exceed industry standards for performance and safety, such as those issued by the Canadian Standards Association and Underwriters Laboratories and include proprietary products for numerous highly engineered applications. These products are used primarily in the North American nuclear and hydro power generation, mass transportation, telecommunications and automation industries.

They have a wide variety of products on both sites. They range from the more commoditized versions of heat shrink tubing (similar to what I have used on my DIY projects) to more complex machines like the one shown below.

This part of the business has tailwinds related to the electronification and connectivity of all things industrial. The have a large presence to the Automotive industry, but it’s data centers, nuclear and related connectivity requirements that have me more excited.

Before the AmerCable acquisition, the prior acquisition in 2022 when they acquired Kanata, a privately owned manufacturer and supplier of specialty cable assemblies and wire harnesses for the nuclear and aerospace industries. The Kanata product lines have since been integrated into the Company’s Shawflex wire and cable business. Katana was acquired for 6.5 million. The terms of the deal were kept private. All we got is that Katana generated 3 million in revenue in the first 9 months of 2022. This would be about 1.6x ttm revenue.

AmerCable

In November 2024 they accounced the acquisition of AmerCable for 280 mil USD (or 390 million CAD). This was about 5x ttm EBITDA. Reverse engineering what has been shared in the segmented results and new mix of total revenue, I get a 1.4x revenue multiple. You can read more about the acquisition here. Here are some specific items from the news release that stood out for me:

Like Shawflex, AmerCable focuses on bespoke, lower volume, higher margin solutions to address complex challenges for which “off-the-shelf” solutions may not be appropriate.

AmerCable will diversify Mattr’s end market exposure with additional material technologies and certifications while enhancing the Company’s raw material procurement scope and efficiency.

The AmerCable acquisition looks to significantly broaden their product portfolio. An example of one of the products that looks fairly simple but is mission critical is the Service Loop cables designed for offshore drilling rigs.

Business Strategy

They have telegraphed some ambitious growth objectives for the business over the next 5 years. This includes doubling revenue by 2030 with a combination of M&A and 10%+ organic growth.

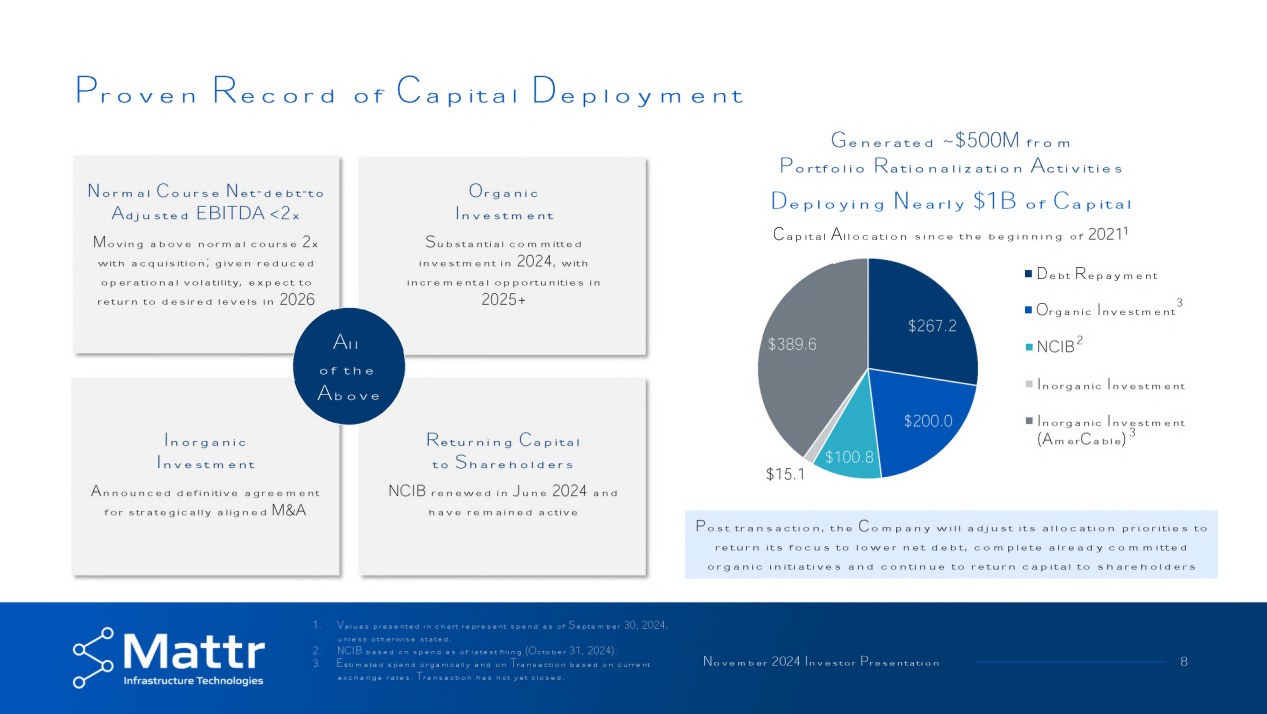

The idea behind MATR is to use the cash generated by the business to grow per share value. This will be accomplished with a combination of opportunistic share purchases, organic growth and some modestly leveraged M&A. So far they have demonstrated this well. The CEO (more on him later) has run a similar play before.

Balance Sheet

They plan to keep debt (excluding lease liabilities) levels under 2x EBITDA. They were there at the end of Q3 2024 even with the acquisition of AmerCable.

The company has invested heavily in the last 2 years via capital expenditures. They are expecting a gradual drop from the 90-100 million annually to the 30-50 million dollar range moving forward. I expect a focus on paying down debt to increase borrowing capacity for some additional M&A.

Share Structure & Ownership

There are currently just under 66 million shares outstanding. Fully diluted there are just over 66 million, so dilution is minimal at these prices.

Turtle Creek owns over 10 million shares. Mawer owns about 3.5 million and Edgepoint owns just under 1.5 million. There are some other institutions with positions but I am happy to be the in company of these three. This brings the institutional ownership ownership to around 30%. I am particularly happy to see Turtle Creek have a position. I have much respect for the Turtle Creek team and what they have accomplished.

Given the market cap, the board still owns less than 1% of the common.

Management & Compensation

Mike Reeves was appointed the CEO in 2021. He has deep industry experience from NOV, Schlumberger and Varel Energy Solutions. He was CEO of Rubicon Oilfield International. Rubicon was co-founded by Reeves and eventually acquired by Innovex in 2021. Rubicon was backed by private equity Warburg Pincus LLC. Rubicon grew to over organically and through quite a few acquisitions. Given the market cap of Mattr corp, I think Mike Reeves is more than qualified to execute on the strategic vision.

There is a great video from Mike Reeves from a few years ago here.

Tom Holloway is Senior VP Finance and CFO. He was CFO of Rubicon Oilfield International among others. Given how much of the future value relies on their ability to understand capital allocation, I am glad to see that the CFO has experience with successful M&A.

Of course, I always wish management owned more stock.

Board

The board has a equity ownership minimum of 3x the director retainer (both cash and equity) within 5 years of being elected. I view this as quite positive for the business. As of last MIC, all directors meet the criteria or are on track. The compensation is mainly share based awards via DSUs based on prior 5 trading days before they are issued.

The board has deep industry experience including:

Kathleen Hall who is a director of Altamont Capital Partners. Altamont is a private equity firm with over 4 billion in assets.

Laura Cillis who was CFO of Calfrac Well Services from 2008 to 2013.

Alan Hibben who is principal of Shakerhill Partners Ltd (advisory and investment company) and is a director of Extendicare Inc.

Katherine Rethy who is a director at Toromont Industries.

Marvin Riley who was CEO of Enpro from 2019 to 2021. He brings experience from General Motors Manufacturing.

Kevin Nugent who is the chair. He currently serves as a director of Hifi Engineering Inc., 8Sigma Energy Services Incorporated, and the Banff Sport Medicine Foundation.

The board is well staffed with a diversity of specialties in my opinion. Given the board members and share ownership from specific funds, I am comfortable with the board’s capabilities with financial markets, operations and capital allocation.

Risks

As with any investment, there are risks. Here are the ones that I have identified:

Key man risk.

I think if Reeves (or Holloway) leaves, I would have to seriously reassess my position in MATR.

Economic sensitivity.

There is no doubt that MATR is tied to the economy. I feel that as long as the economy keeps ticking along, we should see support for the markets that MATR serves.

Major shareholders and liquidity.

This can be a double edged sword. I mentioned there are several well regarded large shareholders. If they decide it’s time to liquidate their position, it would put some serious pressure on the stock price.

Project/backlog issues.

In late 2023 Mattr announced that they have over 27 million in POs for Flexpipe. The work did not materialize and I am not sure what to think about this. Regardless, I thought I would call it out.

Many moving pieces.

With the divestitures, acquisitions and restructuring there are lots of moving pieces here. This can create a fair bit of noise and make it hard for my (limited) cranial capacity to analyze.

Valuation

It’s a bit hard to get a run rate for MATR from here. There is the obvious digestion of AmerCable and normalizing of operations as the streamline operations post the large capital investments made. I have them doing 200-220 in EBITDA moving forward.

This puts them at 5.4x EV/EBITDA (my estimates). With the 70% FCF conversion that works out to about 8x EV/FCF. It’s a discount to peers.

Closing Thoughts

As I mentioned earlier, there have been a few people on X that have said MATR has a similar setup to early days at TVK.to. I honestly don’t know. I think regardless if we get another TVK or not, there is a lot to like at these prices. There are multiple avenues to deploy cash with a management team that has demonstrated strong capital allocation skills.

MATR is also an industrial that has exposure to many parts of the economy that are seeing increased spending like nuclear reactors and data centers.

I think such things limit the downside in the share price.

Having said that, MATR needs to execute from here. The business will need to demonstrate the profitability that they outlined in order to get a re-rating. And if we want to achieve the coveted “compounder” status, we need the business to perform and their capital allocation skills to be top notch.

What do you think about MATR? I would love to hear your opinion.

Thanks for reading my work.

Dean

*disclosure – long MATR

Thanks for the write up. I bought into this in the dark days of the pandemic and sold at around $18. I have just bought back in now. Hopefully the geopolitical situation can cool down a bit.