Measuring Performance

Separating the business, the stock, and portfolio decisions

This post is part of my How I Run My Portfolio series—where I break down how I actually manage my capital. You can find the full series here.

If you are interested in this type of content, consider subscribing.

Introduction

Measuring performance is important.

It is especially important if you are planning on doing this full time one day. If investing is a side quest, then maybe it matters less. But even then, you still need some way to know whether your process is working.

The hard part is that measuring performance isn’t as simple as asking, “Did the stock go up?” or “Am I outperforming?”

Outperforming who or what? Over what time horizon?

Do this long enough and you will experience the following. A stock can go up and I may still have done parts of the job poorly. A stock can go down, and I may have done the job well. This is a world of probabilities. The outcome matters, but so does understanding what caused the outcome.

In order for me to grade myself as objectively as possible, I think there are three roles I need to separate when I measure my own performance:

Stock analyst.

Business analyst.

Portfolio manager.

Each role is quite different and should be measured differently. Each bet and time period requires more or less of some of the roles.

Business Analyst

I need to separate the business from the stock, and that’s what this role is. The business analyst is looking at the company, its competitors, the industry backdrop and whatever macro factors are relevant for this specific business. This is different than looking at the stock. When thinking of this role, I’m trying to answer the following:

My ability to understand the business.

My ability to understand management.

My ability to understand the financials.

My ability to understand the business from an opportunity standpoint.

My ability to understand what could go wrong with the business.

An important distinction is this isn’t business quality. It’s my ability to analyze the business. The important part here is that I can’t use price reaction alone to grade myself. I have seen too many investors use short term price movements to grade management.

How to grade this role

The business analyst question is:

What are/were my expectations for how this business will perform given my time horizon?

Did it perform better or worse than my expectations?

Given the time period, did management navigate things well?

Is the business set up for success in the future?

Being wrong can look like the following:

Maybe I overestimated its durability.

Maybe I underestimated customer concentration.

Maybe I missed balance sheet risk.

Maybe I didn’t understand the competitive environment.

Maybe I assumed management could control something they couldn’t.

I can’t blame the business or management for things they can’t control but I can look to grade them on how they navigate. This role isn’t trying to anticipate things that are inherently unpredictable like if we have a trade war, but it does look to grade how the business navigated it.

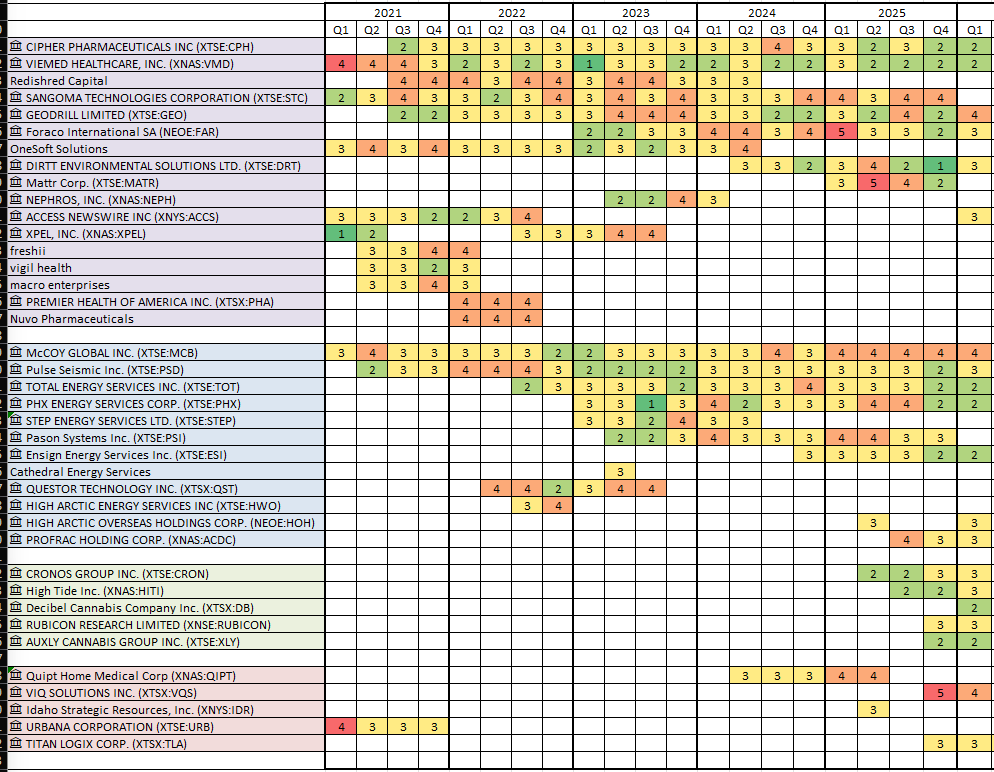

How I grade myself for this role

Every position that I own (and those that I closely follow) I will give each quarter a 1-5 rating. I use this as part of my feedback system to see where my opportunities are.

Challenges in grading

The challenge I have is making sure I properly define business performance over the time period and properly understanding what is in play to grade myself vs what isn’t.

Stock Analyst

The stock analyst is looking at the setup. Or the specific bet given all the information available to me. This is the bird’s-eye view of the situation. I am taking in all the information I have and trying to assess probabilities.

What are the chances this will make money?

How much money can I make if I am right?

How much can I lose if I am wrong?

Is the expected return attractive enough?

Is the valuation reasonable?

What is priced in?

How does this opportunity compare to the market or to other opportunities available to me?

This is where understanding expectations matters.

A company can be good, but the stock can still be a bad bet. A company can be mediocre, but the stock can still be interesting if the price, expectations, and setup are attractive enough.

How to grade this role

As a stock analyst, I am trying to judge the bet.

Did the stock perform relative to the opportunity I thought existed?

Did it perform relative to the market?

Did it perform relative to other things I could have owned?

Was I right for the right reasons?

Sometimes a stock works, but not because I understood it correctly. Maybe the whole sector went up. Maybe liquidity came back. Maybe a multiple expanded for reasons I didn’t anticipate.

I’ll take the win, but I still need to be honest about whether the original analysis was good.

How I grade myself for this role

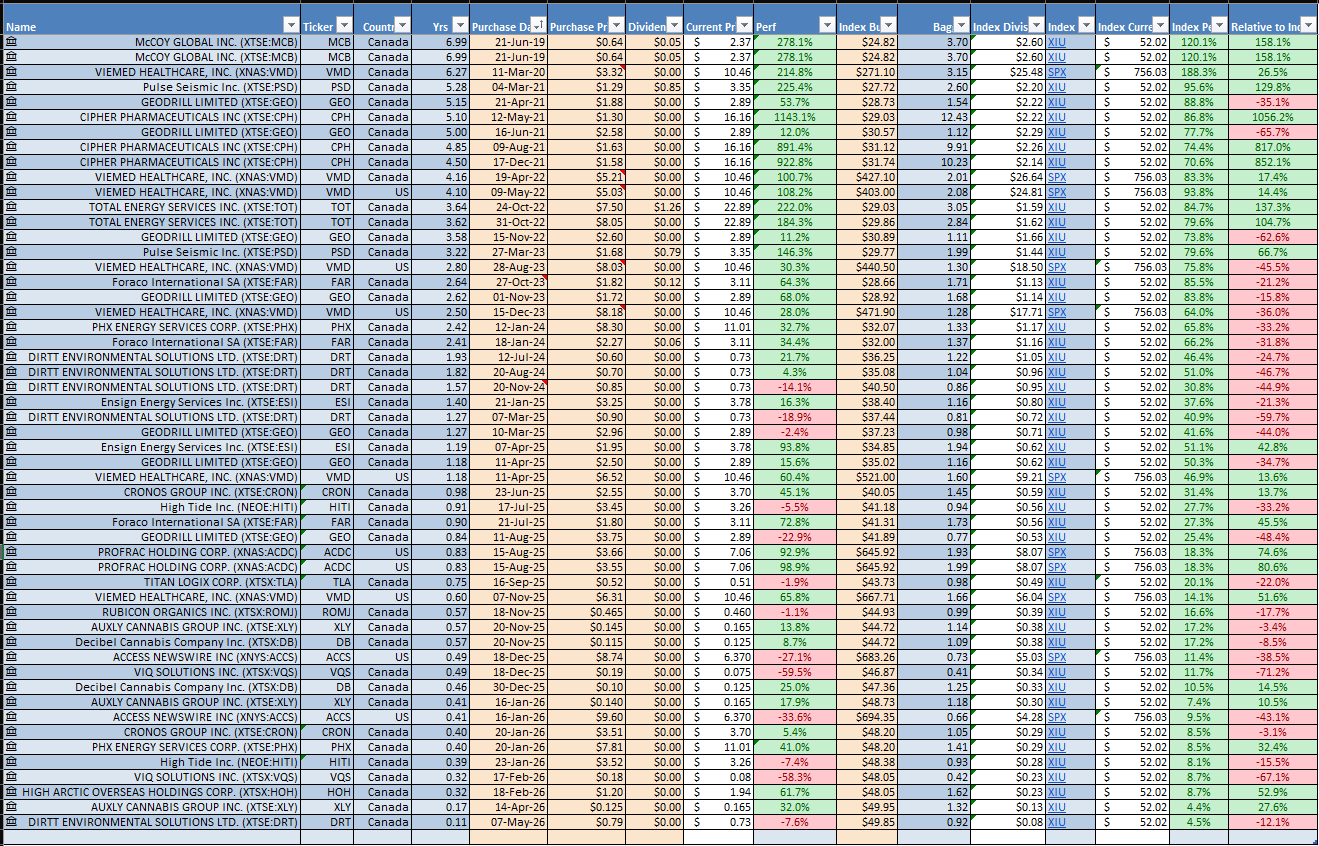

Grading this one can be more straightforward. Did the shares go up or down from when I put capital at risk. Every time I put at least 1% of my capital at risk on a bet I track how it did relative to a benchmark. These are the open/current positions:

The closed positions track the same things but are closed and locked in. I essentially have over 300 micro-trades to use in my feedback system at this point.

Challenges in grading

The challenge can come in if you have loose convictions. Do you track something you only get a partial position in? What happens if something multibags, do you count it as just one bet if you sell some?

These are pretty nuanced questions and probably better answered on an individual investor basis.

Batting Average vs Slugging Percentage

What really drives returns in the long run isn’t having a pick outperform the market by 5%, but my multiples. At least with my style that is the case. Your batting average is important to some degree, but really it’s you slugging percentage. You can batt .500 but underperform the market and you can batt .350 and massively outperform thanks to a high slugging percentage. It’s an important caveat.

Portfolio Manager

The portfolio manager is looking at the whole portfolio in aggregate. This is a different job. I can be right on the business and right on the stock but still manage the position poorly.

Did I size the position appropriately?

Did I add when I should have?

Did I sell when I should have?

Did I hold too long?

Did I let a position get too big?

Did I let losers drag on results?

Did I compare the position against other uses of capital?

A portfolio manager has to think about opportunity cost.

Sometimes I have been too patient with positions that no longer deserved the capital. Sometimes I have let a thesis get stale. Sometimes I have kept waiting for the market to care when I should have moved on.

Other times, I have sold too early or not sized something aggressively enough when the opportunity was clearly improving.

How I grade myself for this role

This grading is reasonably straightforward in the short term. Did the portfolio go up more than my benchmark? It’s really yes or no. You can pick the benchmark for yourself. My thinking of benchmarking is an alternative version of myself and what performance would be. So I track the TSX, Nasdaq and S&P 500. Is it perfect? No.

Challenges in grading

Like the other roles, there are challenges with this one. I need to pick a realistic benchmark. I also need to pick a realistic time horizon. And even then, I have to be mindful of my style. I tend to have long periods of underperformance with short periods of outperformance. So though I track quarterly, it isn’t necessarily fair to grade this role quarterly.

Having said that, I can’t say that after 5 years of underperformance, that my outperformance is around the corner.

A Note on Benchmarking

Benchmarking matters, but I don’t want this post to become a full benchmarking post. I’ll likely write about that separately.

It is obvious that I shouldn’t measure myself against the Dow Jones or the Japanese stock index if those have nothing to do with my actual opportunity set.

The benchmark should be the alternate reality of myself. But the answer also may not be as simple as only comparing myself to the S&P 500.

When I first started investing, I used a mix of what I probably would have purchased if I wasn’t managing the money myself. That included things like the TSX, emerging markets, and the S&P 500.

Today, if I wasn’t doing this myself, I would probably own ETFs. So, I track the larger benchmarks.

Benchmarking against investors

I have found that comparing myself to other investors (mainly anon investors) is a mixed bag. Their results may not be audited. They may use leverage. They may use options or warrants. They may have different timelines. They may be at a different stage in their investing journey. They may only be sharing what they want me to see.

It doesn’t mean it’s a complete waste, but it does have caveats.

I can learn from them.

I can get ideas.

I can get feedback.

I can collaborate.

Bringing the Three Roles Together

Different Bets Weight the Roles Differently

It goes without saying, but different investments required different things from each role.

Sometimes the bet is more about the stock analyst. Other times, it is more about how well I understand the business. I have more experience at understanding certain businesses, and other times I am over my skis.

I used to think valuation mattered more for the stock analyst than the business analyst. I no longer think that’s always true. A low valuation may be a sign of poor sentiment, but it can also push me to understand why one business trades at a lower valuation than another. Sometimes the valuation is cheap because the market is wrong. Sometimes it is cheap because the business deserves it.

Over certain time periods, the portfolio manager role can also dominate results. Concentration, diversification, cash levels, position sizing, and opportunity cost can all drive outperformance or underperformance, even if the individual stock and business analysis were reasonable.

Avoiding Sloppy Conclusions

The main reason I like separating these roles is that it helps me avoid sloppy conclusions. I am looking to grade myself in an objective way in a world full of nuance and probabilities.

If a stock goes up or down, I don’t want to automatically say I did a good or poor job. I need to try and tease out the following:

Maybe the business analysis was poor, but the stock was cheap enough that it didn’t matter.

Maybe the stock analysis was good, but I sized it too small.

Maybe the portfolio management was poor because I sold too early.

Maybe the business performed as expected, but the market didn’t care yet.

Maybe the valuation was too high.

Maybe the position size was wrong.

Maybe the thesis is still intact, but the timeline has changed.

Separating the roles gives me a better way to review my own decisions.

Business analyst: did I understand the business?

Stock analyst: did I understand the setup?

Portfolio manager: did I manage the capital properly?

Those are different questions. They deserve different answers.

My Personal Grade

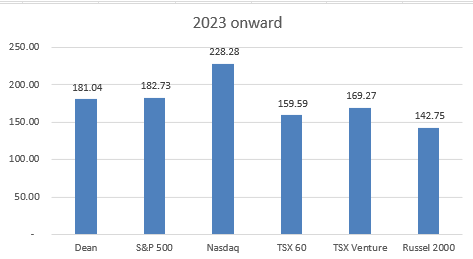

If I was to take a step back or birds eye view, I would give myself the following grade for each role. I have mentioned my time horizon is 9-30 months, so using that I would give myself the following grade:

Business analyst: C

Stock analyst: B

Portfolio manager: C

This would be using 2023 onwards if you put $100 in each. As you can see, I am essentially just keeping pace with the S&P 500.

There have been times when I would grade myself higher, but that is not the case at this point in my journey.

Closing Thoughts

A younger version of myself thought that measuring performance was more straightforward. As I get additional reps in, I find it more nuanced.

The more I do this, the more I think measuring performance properly requires separating the different jobs inside investing. I am an army of one for my portfolio. Labeling these roles helps me compartmentalize my portfolio.

Sometimes I’m acting as a business analyst.

Sometimes I’m acting as a stock analyst.

Sometimes I’m acting as a portfolio manager.

Keeping this separate helps me determine luck from skill, good analysis from good outcomes, and patience from stubbornness.

How do you measure your own performance? Do you separate the business, the stock, and the portfolio decision?

Thanks for reading my work.

Dean

If you found this useful, you can follow the full series here.