November 2020 Update - $CSW/A.to & $CSW/B.to, $OSS.v, $REPH, $PSD.to, $ISV.to $IDG.to, $STC.v, $VMD.to, $SYZ.to, $MCB.to, $FRD, $FRII.to, $MTLO.v

Very busy month. 3 new company's profiled ($MTLO.v, $DWSN, $SVT) and lots of updates.

Let's get to it.

Corby Spirit and Wine Limited (tse: $CSW/A.to & $CSW/B.to)

Reported their fiscal Q1 2021

Strong q

Rev up 12%

Opex down 14%

Net earnings up 68%

Dividend upped to 0.22/share

Yielding almost 6%

They have made notes that they don’t expect this to continue for the full year

Some pull forward for holiday season but higher than prior consumption may continue due to reinstated lockdowns

OneSoft Solutions ($OSS.v)

JV to expand presence in Middle East – find it here

Released Q3

In line with expectations

Rev up sequentially and slightly up yoy

Best MD&A in the Canadian small cap space

New pay as you go sales model being trialed

A few customers in the trial phase – likely to be announced in 2021

Admitted that doubling of 2019 rev won’t happen this year

Recro Pharma ($REPH)

reported results – mixed bag

rev up from Q2 but still down yoy

positive

seeing some wins in business development

some renegotiated of debt to push out current payments and increased flexibility

negative

still no new CEO

still high cost debt

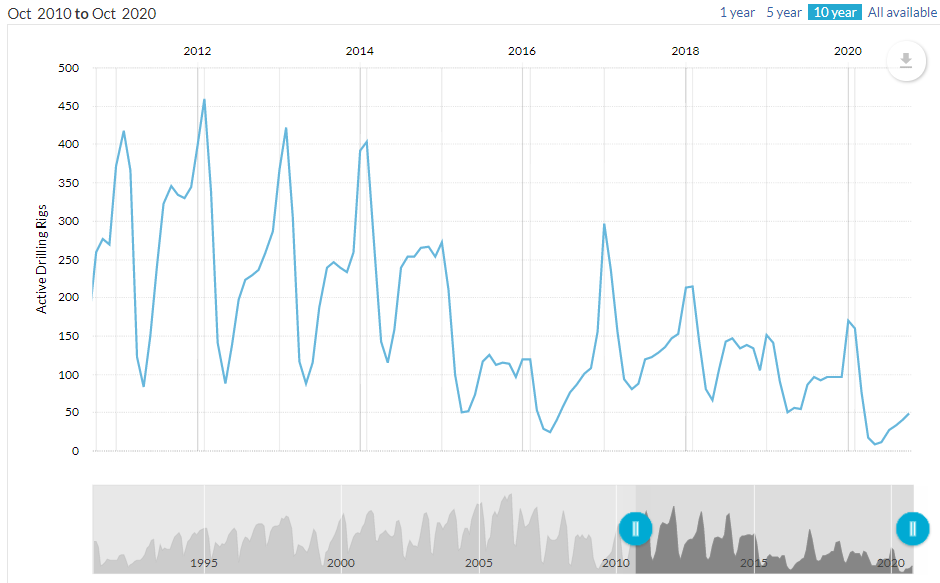

Pulse Seismic ($PSD.to)

reported Q3 and was a tough q

sales down to 1.8mil

still generate 860k for shareholders which shows how little their operating costs are

interesting that they had very little traditional data sale revenue and had a transactional sale

trading at about 50mil MC and a little more than 14x annualized FCF at the most depressed biz environment in the company’s history

You can see how low the active rig count is in Alberta relative to the prior 10 years

Information Services Corp ($ISV.to)

Reported a pretty decent quarter

There was some catch up from previous quarter as the economy in Sask reopened

Trading around 12x EV/EBIT and a little over 4% yield

It will be interesting to see if they do another acquisition in a couple of quarters and/or increase the dividend

Indigo Books & Music ($IDG.to)

Reported fiscal Q2 2021

Results were better than I was expecting

No questions on the call from analysts – I continue to think I’m the only one watching this one

Also announced an addition to the board that seems like a good fit

The holiday quarter is the most important quarter for IDG, it will be interesting to watch as Canada managed the 2nd wave of Covid

Sangoma Technologies Corp ($STC.v)

reported fiscal Q1 in line with expectations

they really are navigating the current environment very well

still looking to deploy cash from recent financing – I’m expecting something soon

Viemed ($VMD.to)

Reported Q3

Revenue was up 22% yoy

Still seeing impact from covid getting into hospitals and preventing new customer wins

Thinking there would have been even more growth if this wasn’t the case

Ancillary sales at 18% and growing fast

I liked how they focus not on incremental gross margin as the ancillary side of the business grows, but incremental gross profit in dollars

Some temporary PPE and equipment sales due to the pandemic

Still see this as a testament to mgmt. being nimble and adapting

Really seeing some gross margin compression

Prepared remarks had dialogue about a potential acquisition

Will be interesting to see if they find a potential company to acquire

They have 32mil in cash at this point

I continue to hold

Sylogist ($SYZ.to)

new CEO announced

seems well credentialed to execute their M&A strategy

McCoy Global ($MCB.to)

New credit facility that gives them some additional flexibility and lower borrowing costs

Released Q3 results

Rev way down

Adj ebitda positive

Backlog stable at 10.6 mil

Continue to wait while things turn around – NCAV is stable to support margin of safety

Friedman Industries ($FRD)

Reported their fiscal Q2 2021

Smaller loss sequentially with some better expectations for Q3

Capital expenditure project costs are coming in higher than anticipated but I do appreciate them investing in the business

Freshii ($FRII.to)

Reported Q3 results

Non event as they are just above EBITDA breakeven

Closed a few more restaurants

Good news is that cash balance (and my margin of safety) is being maintained

Martello Technologies Group Inc ($MTLO.v)

Released fiscal Q2 2021

Numbers were below what the market was expecting and MRR was lower than I thought it would be

I believe there was higher expectation for organic revenue growth

Will keep monitoring the position

Announced a partnership with Rapid Circle (a Microsoft Gold Partner)

Further validates their value to customers in my opinion