Pason Systems Q4 24 Update - $PSI.to

Quick update after Q4 2024

*Disclosure: I own shares in PSI. I am not a professional. Please do your own due diligence.

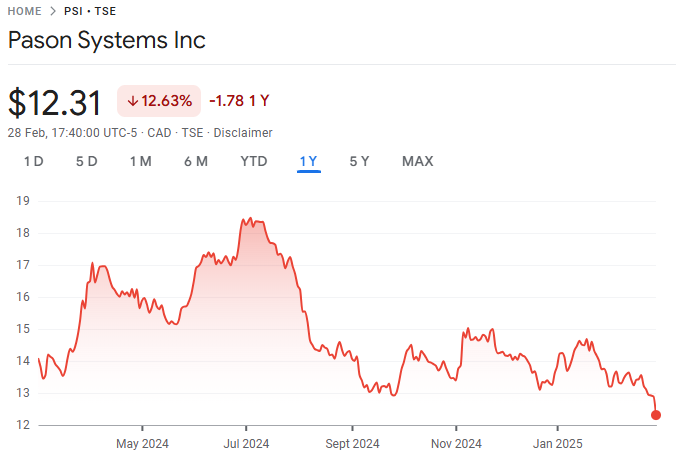

Price: $12.31 CAD (at time of writing)

MC: 982 million CAD

EV: 903 million CAD

Yield: 4.2%

1 year performance: -12.6% (not including dividends)

PSI reported on Thursday and held a call Friday morning. Results were a bit ahead of my expectations. However the stock ended down 4.5% on Friday.

*all numbers in CAD unless stated otherwise

Quarter Recap

Revenue came in at 107.6 million.

Up 15% yoy and 2% sequentially.

EBITDA came in at 42.1 million.

Up from 38.8 million last year.

This is the first full year of IWS results.

North American Drilling:

Revenue up 2% for 71.8 million.

$1,046 revenue per industry day, which is up 5%.

International Drilling:

Revenue at 15 million. Down from 17.9 million last year.

There was quite an impact from FX fluctuations and high inflation in Argentina.

IWS/Completions:

Revenue came in at 13.6 million.

5,668 revenue per industry day.

26 active jobs, which is down from 28 last quarter.

Anticipate 65 million in capex in 2025.

Growth capex focus will be on IWS organic growth and mud analyzer rollout.

At this point, sounds like they expect 2025 to be more or less the same as 2024 from an industry activity standpoint.

Call Notes

Completions:

Still sub-scale.

Need more customers and further adoption of existing to get to better scale and see margins similar to Drilling.

Customer acquisition sounds like it’s going well. The slower ramp seems to be existing customers going with less jobs.

Capex:

65 million total.

Roughly 40 million towards Drilling.

Some maintenance and some growth for Mud Analyzer.

Remaining 25 towards IWS.

Towards valve management and automation technology.

Capital Allocation:

Prefer buyback to large increase in the dividend.

Even with investments in the business, they will still generate cash this year.

Though they like to run at a net cash position, they don’t feel the need to have the same high level of cash as they did previously.

Valuation

I have them at about 6x EV/EBITDA on a trailing basis. It ticks down a bit if we use 2025 EBITDA estimates.

Closing Thoughts

Tailwinds that I see:

North American drilling activity has hopefully bottomed. This is a combination of a more favorable business environment in the US and Canada.

Canada has a likely change at the Federal level this year. And also the provinces have actually been collaborating to reduce interprovincial trade and we may even get some pipelines approved up here.

IWS should have seen activity bottom as well. Nat gas is up from it’s low, but still well below levels a couple years ago.

I see them continuing with a buyback here.

Headwinds:

The tariff talk does not bode well for money moving into cyclical industries.

As well the eventual impact is quite uncertain. And the market hates uncertainty.

Though I am hopeful that we see some EBITDA growth in 2025, I am not sure how much we would get.

PSI has seen it’s valuation compress here. I understand why, but I think it’s reasonable to expect both growth in per share numbers and the multiple over the next couple years.

I like PSI in a basket of OFS cos. I continue to hold my position and look to add on weakness.

Thanks for reading.

Dean

* long PSI.to