Pason Systems Quick Update - $PSI.to

Quick update after Q3 2023

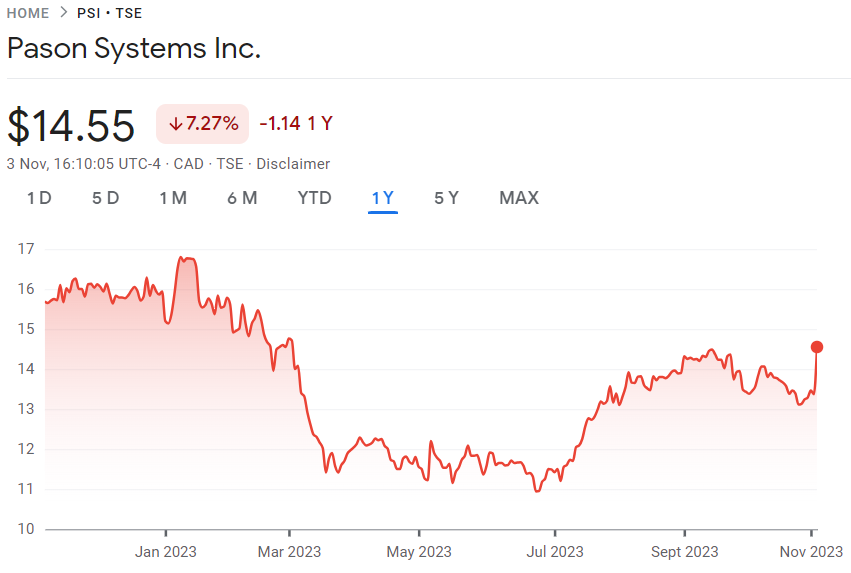

Price: $14.55 CAD

MC: 1.2 billion CAD

EV: 1 billion(ish)

Yield: 3.3%

1 year performance:

PSI reported last night and held a call earlier today. Results were ahead of my expectations and the stock was up about 9-10% during the day.

Quarter Recap

Revenue was up 1% yoy

They managed to offset lower activity by increasing revenue per industry day

North America revenue down 4%

International revenue down 3%

Solar and Energy storage revenue up 293% which made up the decline in the other business segments

EBITDA was down 9% yoy

Continued investment in Intelligent Wellhead Systems (IWS) for 5 mil

Added another 5 mil after end of the quarter

Expecting capex in 2024 to be similar to 2023 (45 million)

Call Notes

There were some interesting comments on the call around their expectations of activity levels and IWS.

IWS comments

They feel the business has lots of opportunity in front of them

IWS is active in every basin

IWS day rate is about 3x the other PSI business but is 1/3 the size

This nets out to about the same size of market

Demand and Outlook

They are expecting activity in the land market to increase moving into 2024

Feel that margins in the last 2 quarters are sustainable

this would be 41-42% ebitda margin

Closing Thoughts

PSI has done well with the lower activity levels. I like their presence in the marketplace. The IWS business allowed them to deploy some capital constructively. The solar and energy storage had a jump in revenue, but given the size of the business at this point the driver will be land activity.

They are trading at a tad under 6x EV/EBITDA and have almost $0.50 per share in cash. I’m expecting a dividend increase and continued NCIB if activity levels remain here or increase.

Thanks for reading.

Dean

* long PSI.to