Redishred Capital Quick Update - $KUT.v

Update after Q1 2023 financials were released

Continuing on with the quick updates….

Business Highlights

Revenue up 36% yoy

EBITDA up 17%

Total system sales up 18%

They are expected a modest paper price decline in Q2

M&A pipeline is strong

Call Highlights

price increases of 4-5% were implemented last year and are taking effect

some route densification opportunities in larger markets

My Thoughts

This was a pretty non event quarter. They are executing as I expected. I think the story still makes sense here though I expected the multiple to be higher. There is a general worry in the market about a recession, rate hikes, war, paper prices, that we are using less paper, when AI will take over and none of this will matter, etc. I have no idea about any of those things. KUT continues to demonstrate strong profitability with a path to being a much larger business on a per share basis.

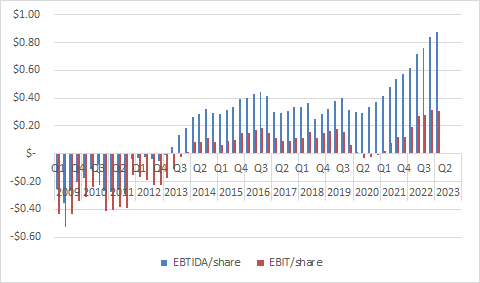

Here is a look at the long term revenue mix and the per share ttm ebit and ebitda.

I continue to hold.

Thanks,

Dean

I might add dilution, debt, and work from home to that list of worries, but at 10% trailing free cash flow yield and ~6x EV/EBITDA vs 12x historically it looks pretty priced in. Same price as the pandemic. I don't really understand. Small caps across the board doing nothing though, might have nothing to do with Redishred. I don't know. Thanks for the post